Aesop's stores look completely different from each other. That isn't design. It's an admission.

Issue #2 · The retailer who treats every store as a piece of architecture, and sells the same fifty products in every one

Walk into the same premium fashion brand in Milan, Munich, and a department-store concession in Madrid. They look the same. Same fixtures. Same lighting. Same product layout. Same SA script, more or less, in three languages.

This is what I think most premium retail CEOs got told twenty years ago, by a consultant in a deck with a lot of arrows: consistency builds the brand. Same store, same experience, same everything, anywhere in the world.

That advice has expired. Most retail CEOs haven’t been told.

The customer who used to walk into the Munich store knowing nothing about the brand, the customer the consistency was designed for, does not exist anymore. By the time they arrive, they have seen the campaign on Instagram, read three reviews, asked a friend, scrolled the e-commerce site, and possibly already added something to a saved cart on Vestiaire. The store is no longer where the brand is introduced. It is where the brand is judged.

Most retail systems have not caught up to this. Buying is still organised store-by-store. The store fit-out budget is still amortised over a uniform rollout. The POS is still optimised to convert a walk-in.

Aesop noticed this earlier than almost anyone. They did something about it. The answer is uncomfortable for any brand still running on a system that was designed for the old customer.

What Aesop actually built

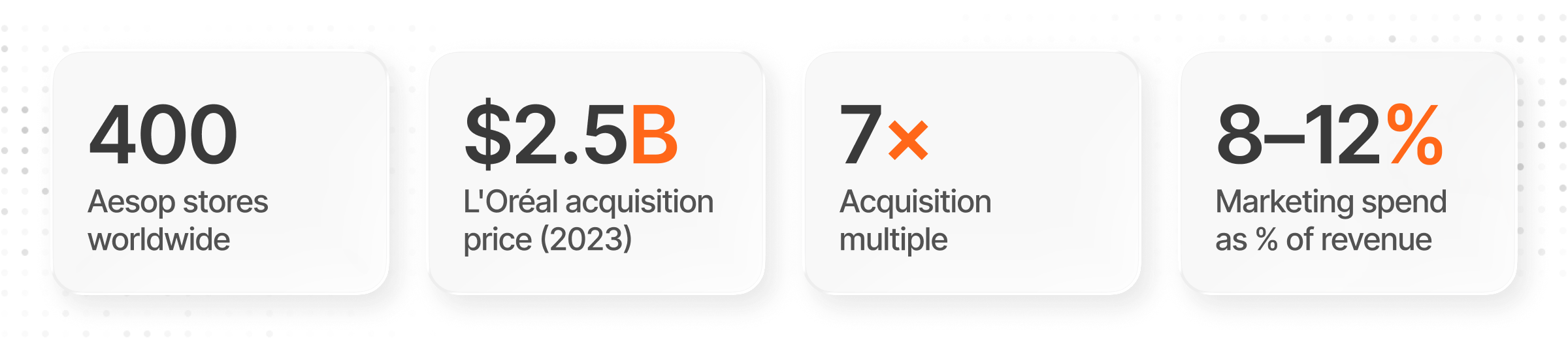

Aesop has roughly four hundred stores around the world. It hires a different architect for each one.

Not a different interior designer. A different architect, often locally famous, sometimes globally so. The Sankt-Peter store in Vienna sits inside an old Catholic confessional. The Park Slope store in Brooklyn is lined with reclaimed copies of The New York Times. The Marylebone store in London is built around a single sink. The Paris Saint-Honoré store is a cabinet of curiosities by Studio KO.

Same product range. Same pricing. Different building, every time.

This sounds expensive. It is, on a per-store basis. What Aesop is paying for is not architecture. They are paying for a reason for someone to walk into the store who already knows what’s inside it.

The acquisition price is the part the industry remembers. It is not the most interesting number. The interesting number is the marketing spend. Aesop appears to spend far less than comparable premium beauty brands on traditional advertising, because the store is the advertising. The architect is the marketing budget. The Instagrammable sink is the campaign.

Why this works, and why your retail director will misread it

The reflex, when a retail director sees the Aesop model, is to file it under “experience retail” and move on. Lovely. Doesn’t apply to us. We have 200 stores and a uniform brand standard.

That reflex is the problem.

Aesop did not invent experiential retail. Lush has a more theatrical store experience. Tiffany has more impressive architecture. Apple’s stores are better attended. What Aesop did is more specific and more strategically interesting.

They decoupled the store from the product. In a conventional retail system, the store exists to sell the product. The store layout, the staff, the music, and the lighting are all in service of conversion. Aesop’s stores are not in the service of conversion. They are in the service of legitimacy. The store’s job is to make the customer believe the brand is worth what it costs. The actual purchase often happens later, online, after the visit has done its work.

They turned each store into a unique cultural artefact. A uniform store rollout has a defined ceiling. Once you have seen one, you have seen all of them, and the store stops being a reason to visit a new city. An Aesop store in Vienna is a different thing from an Aesop store in Sydney. The customer who has been to seven Aesop stores has had seven distinct experiences with the brand, not one experience repeated seven times. That is a fundamentally different relationship.

They made the store carry the brand cost that other companies put into advertising.

Most premium retailers spend 8–12% of revenue on marketing and 5–7% on store fit-out and rent. Aesop inverts the ratio. The store carries the brand-building work that ads do at L’Oréal. The result is a customer who arrives pre-sold and leaves pre-evangelised. The reduced marketing spend isn’t austerity. It’s a redirected budget.

The deeper point should make any premium retailer pause. Most retail systems still treat the store as a unit of distribution. Aesop treats it as a unit of brand-building, and runs a different P&L for each one.

The system most premium brands are running was designed when the store was the first touchpoint. It is now, almost without exception, the last. Almost no operational system has been re-architected to reflect that.

How to build a version of this in your business

You don’t need four hundred stores and a different architect for each. You need to stop running every store on the same template, because the customers arriving at each one are different now.

Audit one store per market against a new question. Pick your flagship in three different cities. Ask, honestly: what is this store for? If the answer is “to drive sales in the catchment,” it is running on the old logic. If you cannot articulate a reason for the customer to walk in that is distinct from your e-commerce experience, the store is a depreciating asset. Most flagships fail this test. The audit takes a day. The result is the most clarifying conversation your commercial team will have all year.

Pick one store in one city to break the template. Not the whole network. Not even the flagship. A second-tier store in a culturally rich city, such as Florence, Turin, Antwerp, Porto, where you can let local context drive the design. Hire an architect, not an interior designer. Give them a brief that says, ” The building should make sense here, and only here.” Run it for twelve months. Compare its repeat-visit rate, its press coverage, and its customer-reported brand affinity to the rest of the network. The numbers will be uncomfortable.

Stop measuring stores only on conversion. A store that converts 15% of foot traffic into transactions but generates no press, no social content, and no customer recall is performing worse than a store that converts 8% but generates twenty press mentions a year. Conversion is a transaction metric. Brand-building stores need brand-building metrics: dwell time, return frequency, organic social tags, press mentions, and the percentage of online customers in that postal code who report having visited. Most CRM systems are not configured to surface these. That is a system problem, not a measurement problem.

Re-cost the store budget honestly. A store fit-out is not a real estate cost. It is a marketing cost in a real-estate wrapper. Move the architectural budget from the property line on the P&L to the brand line. The number will look different to your CFO. It will also be more accurate. The reason your CMO has too small a budget is that half of the marketing spend is hidden in your store accounts, miscategorised.

Accept that uniformity is now a liability. This is the hardest one. The operations team will push back because uniformity is what makes their job easier. Uniform stores are easier to staff, easier to merchandise, and easier to refurbish. They are also less and less interesting to the customer. The operational efficiency of a uniform network is real. The brand cost of it is also real, and it has been quietly compounding.

Uniformity is still being treated as an operational discipline. In many stores, it has become brand erosion.

A soft version of this, one architect-led store, one re-costed P&L, one alternative metric set, will tell you within a year whether your customer responds. Aesop’s customers responded. The retailers who still run identical stores in fourteen cities are not paying attention to who is now walking through the door.

Most are still running stores designed for the old customer. Your system never noticed they stopped showing up.

Retail Ideas · One powerful retail tactic, every week. Written by Susan Jeffers.

— Susan

Reply and say hi. I read everyone.