The Birkin premium is falling. The Hermès thesis is not.

Issue #1.5 · The Hermès numbers softened this winter. Most of the industry is reading the data wrong.

A note on schedule

I publish this newsletter on Mondays. This one is going out on a Wednesday, because something happened in the data this winter that directly tests what I wrote in Issue 1, and pretending it didn’t would be a kind of intellectual cowardice. So.

The Birkin premium is falling. The Hermès thesis is not.

If you read Issue 1, you read me argue that Hermès has built the most disciplined system in luxury retail. A pre-spend ratio. An allocation model. A forty-year refusal to fill demand. And a resale market that does the brand’s advertising for free.

Then, over the autumn and winter, Bernstein Research published a number that the trade press has spent the last two months circulating without quite knowing what to do with.

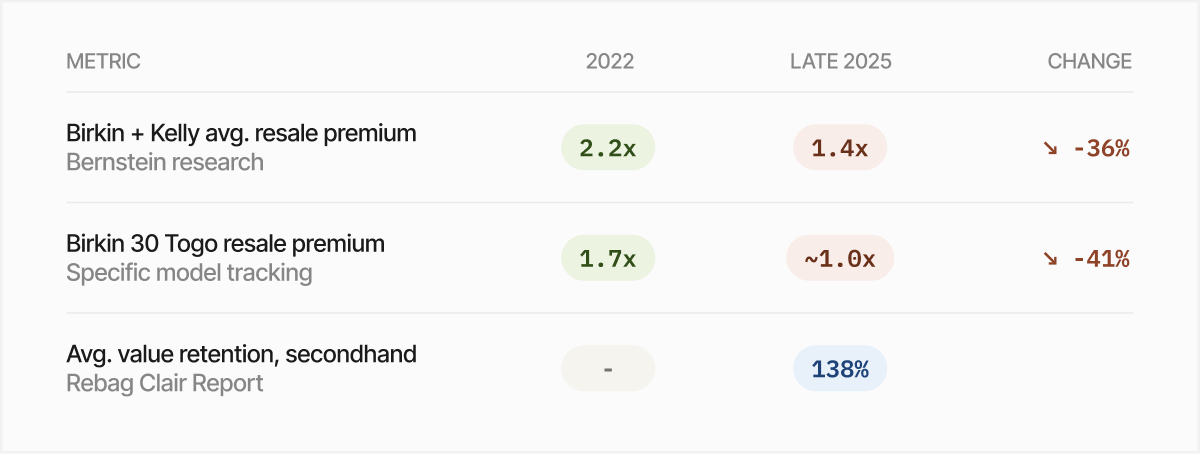

The average resale premium for Birkin and Kelly bags has fallen from 2.2 times its original value in 2022 to 1.4 times as of late 2025. The Birkin 30 in Togo leather, the single most-tracked silhouette in the category, is now reselling at roughly retail. No premium.

This is being read, by people who have not thought about it carefully, as the beginning of the end of the Hermès mechanism.

I think it is the opposite. I think it is the moment the mechanism was built for.

What the data actually says

Three things, none of them what the headlines have been claiming.

The headline is a single number: 2.2× to 1.4×. Read in isolation, it sounds like collapse. Read against the other two numbers, it tells a different story.

First, Hermès is still the strongest brand on the entire secondary market, by a significant margin. A 38% appreciation against retail is what most luxury brands would commit financial fraud to report.

Second, the 1.4× premium is exactly what you would expect a healthy secondary market to look like under tightening discretionary spend. The 2.2× peak in 2022 was, plainly, a bubble. Pandemic excess capital with nowhere to go found its way into hard-asset luxury. That capital has now found other places. The premium has normalised.

Third, and this is the part the trade press has missed: the Birkin 30 Togo specifically, the one that now resells at parity with retail, is also the bag whose retail price rose from $13,900 in 2025 to $14,900 in 2026, a 7.2% increase. A “no premium” Birkin 30 today is selling for almost $1,000 more than a “1.7× premium” Birkin 30 in 2022, in dollar terms. The premium fell. The absolute price did not.

What’s happening is not the collapse of the mechanism. What’s happening is that the speculative layer on top of the mechanism is being repriced.

Why this matters for everyone else

This is the part that should make any premium retail CEO sit forward.

For the brands underneath Hermès in the desirability hierarchy, the brands that do not have a pre-spend system, do not have allocation discipline, do not have a forty-year track record of refusing to make more, the same macro pressure that lowered Birkin’s premium from 2.2× to 1.4× is doing something far more violent to their economics. It is just doing it more quietly.

A Birkin going from a 2.2× resale premium to a 1.0× resale premium is a story. A premium fashion brand going from full-price sell-through of 78% to 61% is not. It is a quarterly metric in a board pack. Nobody outside the company sees it. The CFO knows. The CEO knows. The merchandising director has been told three times this year.

The mechanism Issue 1 described was not built to maximise upside in a luxury supercycle. It was built to survive the inevitable correction. 2025 marked the end of what Berenberg analysts have been calling the luxury supercycle, as consumers face inflation headwinds and retailers fail to woo aspirational shoppers.

The brands with allocation discipline are now experiencing margin pressure on the speculative layer above their floor. The brands without it are experiencing margin pressure on the floor itself.

That distinction is the whole story.

What this changes about the playbook

It doesn’t.

The playbook I described in Issue 1, gate one hero SKU behind relationship depth, hold the line on supply, protect the system from your own commercial team, is the playbook for both halves of the cycle. The brands that built it before 2022 are now experiencing the version where they keep most of their pricing power while the air leaves the speculative top of their market. The brands that did not build it before 2022 are now experiencing the version where the speculative top, the floor, and the wholesale partners all soften at the same time, while the off-price channel quietly opens up to take inventory the retailer cannot move.

There are two different conversations being had in luxury boardrooms this quarter, and they are not connected. One conversation is “are we worried about Birkin?” The other is “are we worried about us?”

The answer to the second question, for almost everyone except Hermès, is yes. The answer to the first question is not the question.

The line nobody is saying

Wealthy shopping unaffected by COVID-related economic woes drove the 2022 premium. That money is now finding harder, more conservative assets. The aspirational consumer that fuelled the long tail of luxury growth from 2021 to 2024 has retreated. Most of the industry, including the trade press, is talking about this as a luxury problem.

It is not a luxury problem. It is a premium-without-discipline problem.

Hermès is the brand the data is being collected on because it is the easiest to measure. The story it is telling is not about Hermès. It is about every brand sitting in the tier below Hermès that built its growth model on the assumption the aspirational consumer would keep showing up. That consumer has gone. The mechanism that made it survivable was built decades ago, by one Parisian house, with absolute discipline.

You won’t build it before the next correction. You will build it after.

That is the most expensive sentence in this newsletter.

— Susan

Reply and say hi. I read every one.